Exploring How HAQQ Brings Shariah Compliance to DeFi

Over the years, Islamic finance has grown, fueled by escalating interest in risk-sharing financial instruments. A blend of features has underpinned the expansion and resilience of Islamic finance, fostering an industry that has grown at an annual rate of 10-12%, with its Sharia-compliant assets currently estimated at just over $1.5 trillion.

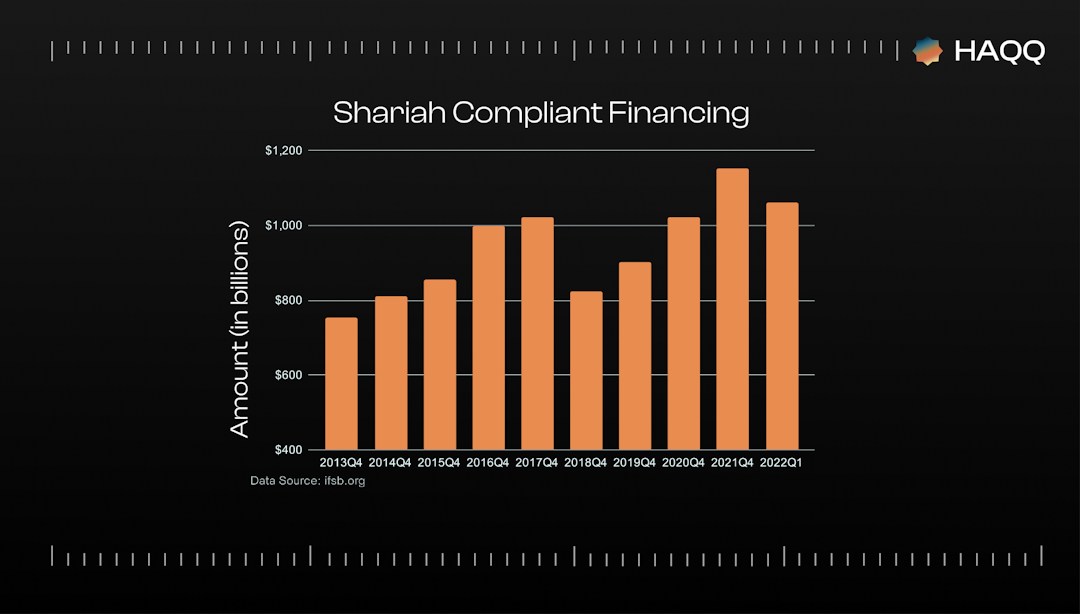

(Image details: The provided data for total assets, total Sharīah-compliant financing, and total funding/liabilities are aggregated from 26 countries, using the structural data of Islamic banks and Islamic banking windows of conventional banks, converted into U.S dollars at end-of-period exchange rates. Data availability varies, with some countries like Iran, Kazakhstan, and Morocco only up to certain quarters, and significant data gaps post-2018 Q4, notably from Iran, which had substantial contributions to the Islamic banking sector.)

On the other side, decentralized finance (DeFi) is disrupting the financial ecosystem with its promise of a decentralized, peer-to-peer network that aims to improve financial inclusion and foster efficient markets. However, DeFi has suffered from crypto scams, causing losses of $329 million in Q1 2022 alone. Islamic finance presents a solution with its risk-sharing, ethical principles.

Enter HAQQ!

Unlike the broader DeFi landscape, HAQQ applies the ethical tenets of Islamic finance to reduce the risk of fraud and exploitation. In our previous blog post, we introduced you to this innovative platform. Today we’ll delve into the core principles of Islamic finance and demonstrate how HAQQ is optimally positioned to develop Shariah law-compliant solutions that cater to the global Islamic community's financial needs.

Deep Dive into Islamic Finance Principles

The Evolution

Islamic finance, deeply rooted in the principles laid down in the Qur’an and the Hadith (sayings and actions of Prophet Muhammad), has seen a remarkable evolution over the centuries. Over the centuries, the principles of Islamic finance remained consistent, promoting ethical and fair transactions. However, the modern concept of Islamic finance began to take shape in the mid-20th century. The broader Islamic revival movement and the desire of Muslim-majority countries to align their economic systems with Islamic principles catalyzed the resurgence of Islamic finance. The first Islamic bank, the Dubai Islamic Bank, was established in 1975, marking the beginning of a new era for Islamic finance.

Adapting Islamic finance to the modern financial world involved a process of innovation and transformation. Islamic financial institutions took the initiative to design financial products and services that not only adhered to Islamic principles but also fulfilled the complex needs of modern economies. As a result, a wide array of Islamic financial instruments have developed, ranging from simple profit-and-loss sharing arrangements (Musharaka and Mudarabah) to more complex structures like Sukuk (Islamic bonds) and Takaful (Islamic insurance). The emergence of Islamic finance in the global market also necessitated the development of regulatory frameworks and supervisory bodies to ensure Sharia compliance. This led to the establishment of organizations like the Accounting and Auditing Organization for Islamic Financial Institutions and the Islamic Financial Services Board.

Islamic Finance vs Conventional Finance

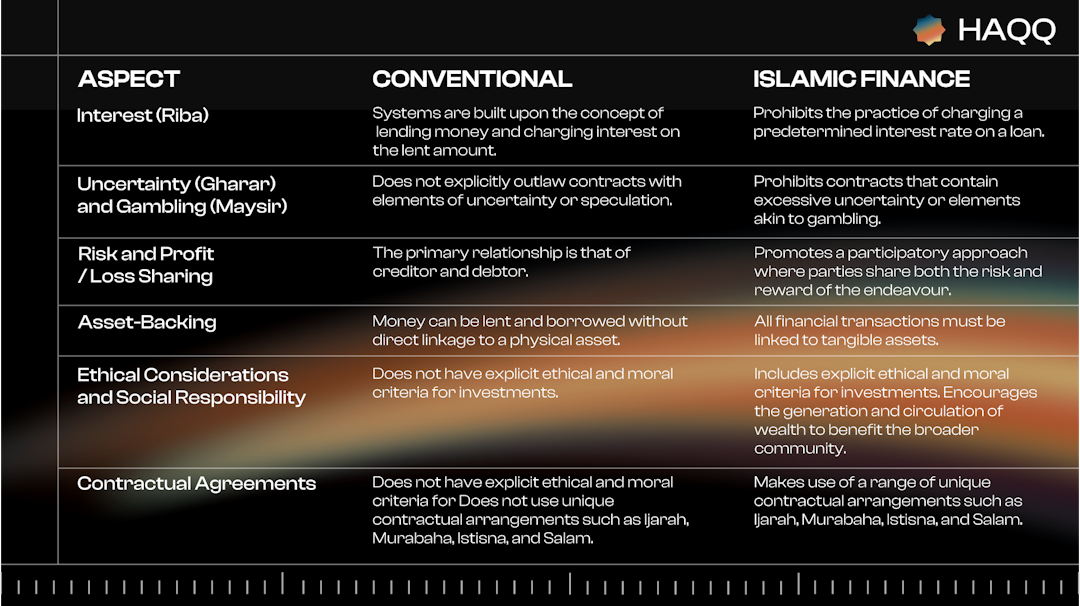

There are fundamental differences between Islamic and conventional finance. The prohibition of Riba eliminates the concept of interest, making all transactions in Islamic finance trade-based rather than credit-based. The prohibition of Gharar ensures contracts are free from deceit and uncertainty. The exclusion of Maysir provides that Islamic financial transactions do not involve unnecessary risk, likened to gambling.

Unlike conventional finance, which emphasizes creditworthiness and interest, Islamic finance emphasizes ethical investment, social welfare, and risk-sharing. In contrast to traditional banks that make money by charging interest on loans, Islamic banks operate on a profit-and-loss sharing model. Essentially, the bank and its customers become "partners" in the financial transaction, sharing the risks and rewards.

Rooted in Asset-Backed Financing

The traditional Islamic financial tools, consisting mainly of basic lending and borrowing mechanisms based on profit-and-loss sharing principles, have evolved into a comprehensive range of financial products and services. However, in Islamic finance, every financial transaction must be linked to a tangible asset, emphasizing the principle of asset-backed financing. This principle resonates with the timeless Prophetic maxim, 'the benefit of a thing is a return for the liability for loss from that thing,' implying that the party enjoying the full benefit of an asset should bear the associated risks.

The performance of Islamic finance is intrinsically tied to the real economy, a connection that served Islamic banks well during the 2008 financial crisis. Their limited exposure to tangible assets shielded them from the fallout of toxic assets and subprime mortgages that impacted conventional banking. Asset-backed financing promotes a flexible adjustment mechanism in the face of unanticipated shocks, keeping the actual value of assets and liabilities equal. This discourages excessive risk-taking and avoids the complications of over-securitization. Whether in partnerships where both parties contribute capital and share management (Musharakah), or contracts where one party supplies the capital and the other works with it (Mudarabah), the emphasis remains on fair risk allocation. This model inherently discourages short-term excessive risk-taking, fosters careful evaluation of funding requests, and creates a conducive environment for navigating tough financial times.

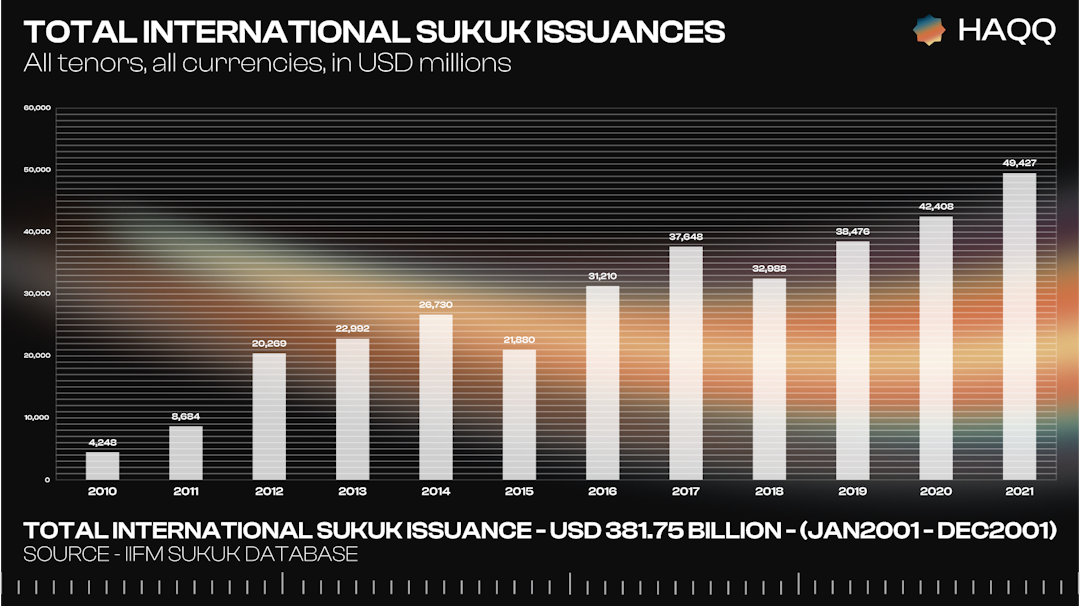

Islamic financial instruments like Sukuk and Takaful demonstrate the adaptability of Islamic finance. Unlike conventional bonds, Sukuk represents ownership in a tangible asset, business, project, or investment activity. Conversely, Takaful is a system of Islamic insurance based on the principle of mutual assistance. The Sukuk market grew from $5 billion in the 1980s to about $1 trillion by 2010, dominated by Malaysia. Unlike conventional bonds, Islamic Bonds are tied directly to assets and adhere to principles of risk sharing. They gained popularity due to their stability during the 2008 financial crisis and have become an alternative, ethical financing solution for various requirements, including corporate needs, project financing, and liquidity management. Despite some fluctuations, the market's growth trajectory continues, increasingly integrating environmental, social, and governance (ESG) considerations. Even with a slight decline in short-term Sukuk issuances in 2021, the market remains stable, with projections for continued growth in 2022.

Is DeFi Shariah Compliant?

Only HAQQ brings Shariah compliance to DeFi.

To ensure Shariah compliance in DeFi, HAQQ has established specific measures and systems. This includes the implementation of the Shariah Oracle and adherence to a Fatwa issued by our IslamicCoin Shariah Board. These measures ensure HAQQ operates within the boundaries of Islamic principles while fully embracing the benefits and potential of DeFi. In the past, we’ve explored the role of the Shariah Oracle. Now let’s delve into the role the Shariah Board plays and the implications of the Fatwa.

The Shariah Board

A Shariah Supervisory Board (SBB) is essential to any Islamic Financial Institution (IFI). The Board ensures its operations align with the principles of Shariah law while also overseeing, guiding, and enforcing alliance with Islamic ethical standards. A Supervisory Board is not merely an advisory body but an integral part of the institution's governance structure, ensuring all transactions and operations are Shariah-compliant.

SSBs utilize a collective interpretative process called ijtihad, which involves independent reasoning based on the Quran, Hadith, and other Islamic legal principles. The board's decisions, known as fatwas, guide HAQQ."

Our SBB, the IslmaicCoin Shiarah Board, includes prominent Shariah scholars like Sheikh Dr. Nizam Mohammed Saleh Yaquby, Sheikh Dr. Mohamed Zoeir, Sheikh Dr. Essam Khalaf Al-Enezi, Sheikh Mohamed Fathiddin Beyanouni, and Sheikh Mohamed Abdel Hakim Mohamed. These individuals have been instrumental in the development and progression of Islamic finance. Their contributions, drawn from a wealth of knowledge and experience in Shariah law and finance, have greatly enhanced the credibility and robustness of the Islamic financial system. Details on each member of our Shariah Board can be found here.

Fatwa

A Fatwa issued by our Shariah Authority has reviewed and validated our approach. The Fatwa examined the establishment of HAQQ, the issuing IslamicCoin (our currency), and our Evergreen DAO Endowment Fund. It concluded that there is no objection to these aspects, provided that we follow specific measures. This includes ensuring that an accredited audit company audits the code used to build the platform and that an Authority committee oversees the activities of the Evergreen DAO Endowment Fund. The Fatwa also emphasizes that the Authority's opinion is strictly limited to these aspects, and any new smart contracts built on the platform must obtain the Shariah Authority's approval before launching. Read the Fatwa in its entirety here.

Conclusion

Our distinctiveness lies in blending the principles of Islamic finance with DeFi and fostering ethical, risk-sharing, and inclusive financial ecosystems. With a deep understanding of the economic aspirations of the global Muslim community, we uniquely position ourselves to architect robust, Sharia-compliant solutions.

As you navigate the world of DeFi, HAQQ offers the promise of a journey anchored in ethics, fairness, and trust. As you embark on this journey, the HAQQ Wallet will be your trusted companion, facilitating secure and efficient transactions in Sharia-compliant DeFi. We encourage you to dive deeper into our blog post detailing the workings of the HAQQ Wallet, arming you with the knowledge to explore this space confidently.